Trust Audit

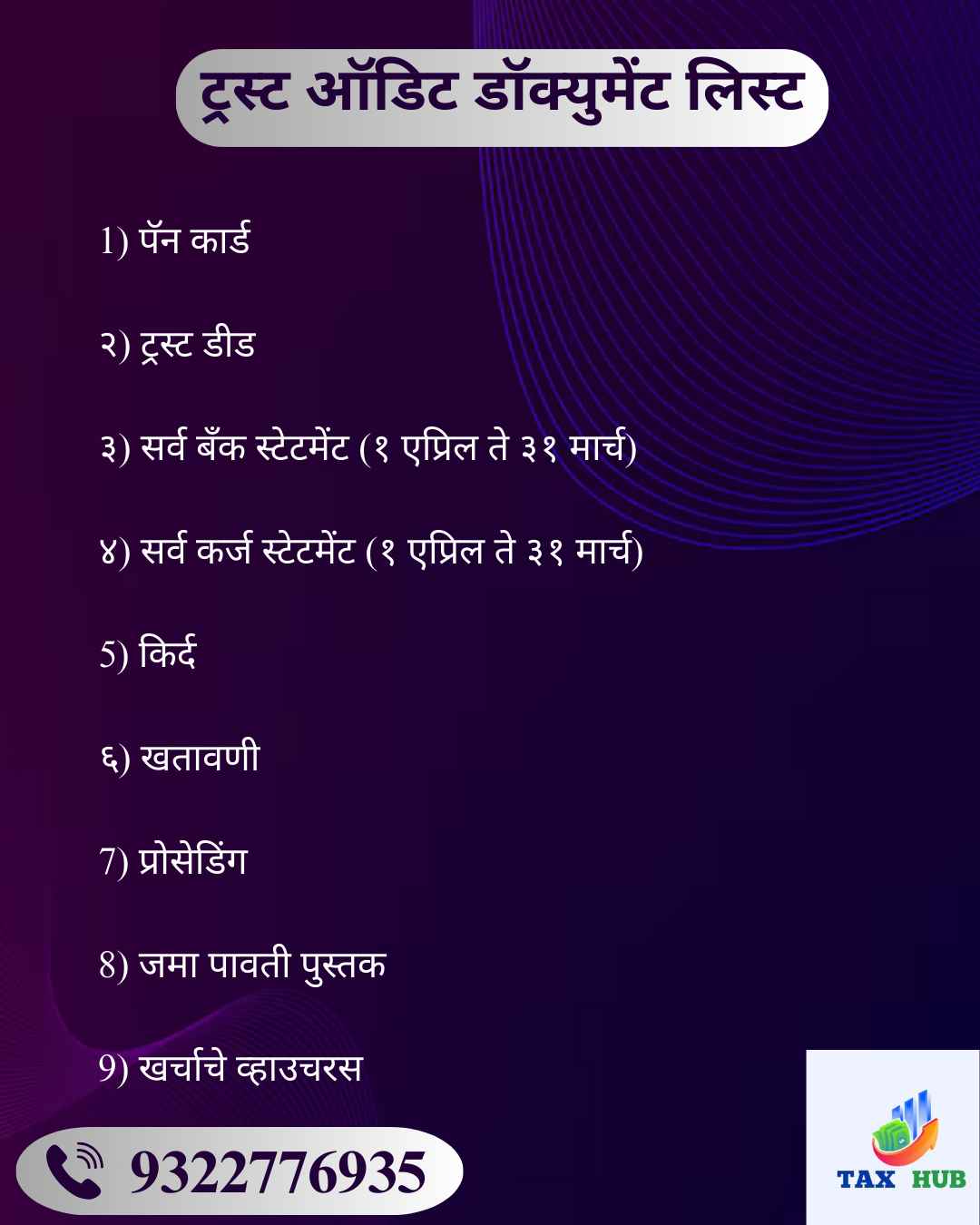

A Trust Audit is a systematic examination of the financial records, accounts, and activities of a trust to ensure transparency, accountability, and compliance with legal requirements. It is conducted by a qualified Chartered Accountant or auditor who reviews the trust’s income, expenditure, assets, liabilities, donations, grants, and utilization of funds. The main purpose of a trust audit is to verify whether the funds have been used for the objects of the trust, in accordance with the provisions of the Trust Deed, the Income Tax Act, and other applicable laws. During the audit, the auditor checks vouchers, receipts, bank statements, and investment details to ensure accuracy and authenticity. For charitable and religious trusts, annual audits are mandatory under most state trust acts and also required under Section 12A and 80G of the Income Tax Act to claim tax exemptions and benefits. An audit report in the prescribed form (such as Form 10B in India) is submitted to the income tax authorities to certify the financial performance and compliance status of the trust. A proper audit not only builds credibility among donors, beneficiaries, and government authorities but also helps detect errors, frauds, or mismanagement at an early stage. Therefore, trust audit plays a vital role in maintaining financial discipline, safeguarding public money, and strengthening the overall governance of the organization.

Advantages of Trust Audit

Financial Transparency

Audit ensures that the trust’s financial records (income, expenses, assets, liabilities) are accurate and genuine.

Builds confidence among donors, beneficiaries, and regulators.

Legal Compliance

In India, registered trusts (especially charitable and religious trusts) are often required to get their accounts audited under the Income Tax Act or the Trust Act (depending on the state).

Audit ensures compliance with all relevant laws, preventing penalties or legal issues.

Improved Credibility

An audited trust gains credibility with stakeholders (government authorities, banks, corporate donors, and the public).

It becomes easier for the trust to receive CSR funding, grants, and donations.

Detection of Fraud & Misuse

Auditors can identify any misuse of trust funds, fraudulent activities, or mismanagement.

Protects trustees and beneficiaries from financial irregularities.

Better Financial Management

Audit reports provide insights into unnecessary expenses, unutilized funds, or scope for better fund allocation.

Helps trustees make informed financial decisions.

Eligibility for Tax Exemptions

Trusts often enjoy exemptions under Section 12A, 80G of the Income Tax Act.

To maintain these benefits, audited financials are mandatory.

Accountability to Beneficiaries

Audit assures beneficiaries and donors that the trust’s resources are being used for the intended social/charitable purpose.

Disadvantages of Trust Audit

Cost Factor

Professional audit services can be expensive, especially for small trusts with limited funds.

Time-Consuming Process

Collecting documents, preparing accounts, and coordinating with auditors requires time and effort from trustees.

Complexity of Compliance

Trusts operating across states or with multiple sources of income may find audits complicated due to different legal requirements.

Disclosure of Sensitive Information

Audits involve disclosure of complete financial details. Some trustees may feel a loss of financial privacy.

Dependence on Auditor’s Efficiency

If the auditor lacks expertise in handling charitable trusts, errors may occur, which can affect compliance and credibility.

Fear of Penalties on Detection

If the audit uncovers irregularities or violations, the trust may face legal consequences, penalties, or loss of tax benefits.

Administrative Burden

For small trusts, maintaining detailed records and accounts for audit purposes can be a heavy administrative load.

Types Of Trust

1. Based on Purpose

Private Trust – Created for the benefit of specific individuals (e.g., family members, relatives). Governed by the Indian Trusts Act, 1882.

Public Trust – Created for charitable or religious purposes, benefiting the general public. Governed by state-specific Public Trust Acts (like Maharashtra Public Trusts Act).

Mixed Trust – Has elements of both private and public trust (e.g., partly for family benefit and partly for charity).

2. Based on Creation

Express Trust – Clearly created by the settlor through a written document or deed.

Implied Trust – Not formally declared but inferred from the conduct or circumstances.

Constructive Trust – Imposed by law to prevent unjust enrichment or fraud.

3. Based on Duration

Revocable Trust – Settlor can alter or revoke the trust during their lifetime.

Irrevocable Trust – Once created, it cannot be changed or canceled by the settlor.

4. Based on Beneficiaries

Charitable/Religious Trust – For the welfare of the public, education, healthcare, religion, etc.

Special Trust – For specific purposes like supporting handicapped persons, scholarships, etc.

Discretionary Trust – Trustees have discretion to decide which beneficiaries get benefits and in what proportion.

Determinate/Specific Trust – Beneficiaries and their share are clearly defined in the trust deed.

Eligibility Criteria for Trust Registration

✓ A minimum of two persons are required to come together to create a trust.

✓ The establishment of the trust must comply with the provisions of the Indian Trusts Act, 1882.

✓ None of the members or trustees should be legally disqualified under any existing Indian law.

✓ The purpose of setting up the trust should not violate any statutory provisions.

✓ Trustees must perform their duties with honesty, fairness, and integrity.

✓ The objectives of the trust must not be against public welfare or any other applicable regulations.

✓ The trust’s functioning should not result in harm or injury to any person.

✓ All operations of the trust should remain consistent with the goals outlined in the trust deed.

✓ The trust deed should be carefully drafted to reflect the genuine intentions of the founders.

✓ If a trust is created with multiple objectives, all of them must be lawful. A trust cannot exist if even one of the purposes is unlawful, even if the others are valid.

Contents of a Trust Deed

A trust deed is a vital legal document that specifies the essential elements and rules governing a trust. It generally includes the following provisions:

◼ The duration or validity period for which the trust will function.

◼ The official registered address of the trust.

◼ The specific region or jurisdiction where the trust will undertake its activities.

◼ The mission, objectives, and purposes for which the trust has been established.

◼ Particulars of the settlor (the person forming the trust) along with details of the assets or property contributed to the trust.

◼ Information regarding the trustees, such as their number, eligibility, appointment, and tenure.

◼ The powers, duties, and responsibilities assigned to the trustees.

◼ The procedure for making amendments to the deed, as well as the rules relating to dissolution or winding up of the trust.

You May Also Like

Niti Ayog Registration

Rs 5000

Trust Audit Services

Rs 3000

12A 80G Registration ( Provisional )

Rs 5000