Accounting Concepts and Principles (GAAP/IFRS)

Accounting Concepts and Principles (GAAP/IFRS)

Accounting is governed by a set of standardized principles and concepts that ensure consistency, transparency, and comparability of financial statements. Two major frameworks followed worldwide are:

GAAP – Generally Accepted Accounting Principles (primarily used in the United States)

IFRS – International Financial Reporting Standards (used in over 140 countries globally)

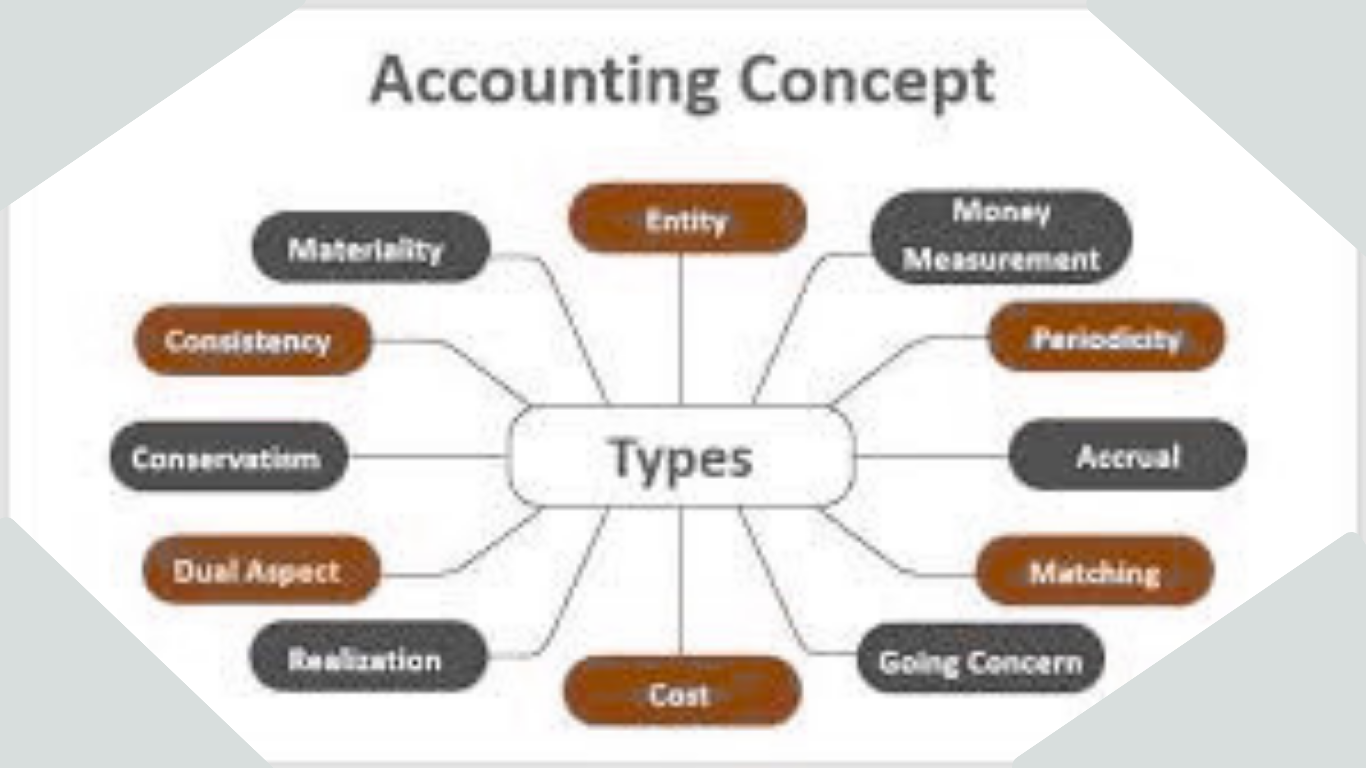

1. Fundamental Accounting Concepts (Both GAAP and IFRS)

Concept Explanation

Accrual Concept Revenues and expenses are recorded when they are earned or incurred, not when cash is received or paid.

Going Concern Assumes the business will continue to operate indefinitely unless there is evidence otherwise.

Consistency Accounting methods should be applied consistently from one period to another.

Materiality Only information that would influence decisions needs to be disclosed.

Conservatism (Prudence) Record expenses and liabilities as soon as possible, but revenues only when they are certain.

Matching Principle Expenses should be matched with the revenues they help to generate in the same period.

Entity Concept The business is treated as a separate entity from its owners or stakeholders.

Monetary Unit Assumption Transactions are recorded in a stable currency without adjusting for inflation.

Time Period Assumption Financial reporting should be done for specific periods (monthly, quarterly, annually).

2. GAAP (Generally Accepted Accounting Principles)

Key Characteristics:

Rule-based system

Established by the Financial Accounting Standards Board (FASB)

Widely used in the United States

Key Principles of GAAP:

Revenue Recognition Principle

Expense Recognition (Matching) Principle

Full Disclosure Principle

Cost Principle – Assets are recorded at historical cost, not fair value.

Objectivity Principle – Use of verifiable, objective evidence in financial records.

3. IFRS (International Financial Reporting Standards)

Key Characteristics:

Principle-based system

Developed by the International Accounting Standards Board (IASB)

Aims for global consistency in financial reporting

Key IFRS Features:

Greater focus on fair value over historical cost.

Emphasis on the substance over form principle: economic reality takes precedence over legal form.

Flexibility in judgments and estimates, which enhances comparability and transparency.

4. Key Differences: GAAP vs. IFRS

Feature GAAP IFRS

Approach Rule-based Principle-based

Inventory Accounting Allows LIFO and FIFO Does not allow LIFO

Revaluation of Assets Not generally allowed Allowed under specific standards

Development Costs Expensed Can be capitalized if criteria met

Extraordinary Items Separate reporting allowed Not permitted

5. Importance of These Concepts and Principles

Ensure Transparency: Stakeholders can trust the financial health of the business.

Enable Comparability: Makes it easier to compare performance across time and entities.

Support Compliance: Helps organizations stay within legal and regulatory bounds.

Assist Decision-Making: Accurate financial reports guide investors, lenders, and management.